The economy’s roller-coaster ride continues. Last year ended with a thud, with consumers retrenching, inflation receding and financial markets slumping. Recession fears became more pronounced as did expectations the Federal Reserve would soon pause its aggressive rate-hiking campaign to prevent a deep slump that would throw millions of workers on to the unemployment lines. Fast forward to this year, and the script has been flipped 180 degrees. The economy appears to be racing out of the starting gate; job growth soared in January, driving unemployment down to a 53 year low; consumers regained their spending mojo, and, most important, the inflation dragon is spewing more fire.

Unsurprisingly, hopes the Fed would soon take its foot off the brakes has all but vanished. Most investors had, until recently, fully believed the Fed would be cutting rates later this year in response to weak conditions and rising unemployment. Now traders are pricing in more rate hikes than the Fed itself had forecast in December.  But the financial markets are also warning of a dire outcome; with short-term rates exceeding long-term yields by the widest margin since the 1980’s, this so-called inverted yield curve is signaling a recession within the foreseeable future. The implication is that the Fed’s tough anti-inflation rate hikes will go too far, sending the economy into a tailspin that will lead to much lower interest rates down the road.

But the financial markets are also warning of a dire outcome; with short-term rates exceeding long-term yields by the widest margin since the 1980’s, this so-called inverted yield curve is signaling a recession within the foreseeable future. The implication is that the Fed’s tough anti-inflation rate hikes will go too far, sending the economy into a tailspin that will lead to much lower interest rates down the road.

We agree that a recession – though a mild one—is likely to occur later this year. But the vigor shown in January’s jobs and retail sales reports has emboldened some to believe that the Fed can restore price stability without sending the economy into a downturn. That’s possible, but such an outcome following an extremely aggressive rate-hiking campaign and steeply inverted yield curve would defy history. More than likely, the early-year growth and inflation spike is another bump in the road that has been a common feature of this erratic post-pandemic recovery. Importantly, the Fed says its rate setting decisions will depend on incoming data. In a highly volatile data environment, the central bank may be embarking on a risky strategy that relies on misleading information.

January’s Upside Surprises

Over most of the second half of last year, hopes were high that the Fed’s inflation fighting strategy was bearing fruit. The most optimistic scenario the central bank hoped for would be an economy that gradually slowed, but not go into reverse, while inflation steadily cooled towards its 2 percent target. That journey seemed to be well underway. Employers stepped back from the frenzied hiring pace seen earlier in the year, consumer spending tapered off and, most importantly, inflation retreated from a peak 9.1 percent in June to 6.6 percent in December. There was still more work to do, but the Fed predicted in December that one or two more rate hikes would do the job, marking the end of the most aggressive rate hiking campaign since the 1980s.

There was still more work to do, but the Fed predicted in December that one or two more rate hikes would do the job, marking the end of the most aggressive rate hiking campaign since the 1980s.

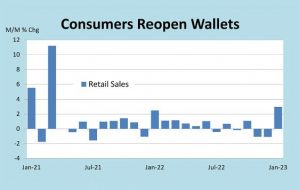

But like many well-laid plans, this one appears to be coming off the rails as the curtain rises on 2023. Job growth picked up in January, with more than half-million workers added to payrolls – the most in six months – consumers flocked back to stores after a soft holiday shopping season, spurring the strongest January gain in retail sales in nearly two years, and inflation, as measured by the consumer price index, staged its largest increase in seven months, jumping by half-percent following a slim 0.1 percent increase in December.

The resurgence of activity and inflation out of the gate this year has upended expectations. Investors that were skeptical of the Fed’s intentions late last year now believe it will go even further than monetary officials predicted in December, sending market yields sharply higher in February. For its part, the Fed is sounding a more hawkish tone than it did at the start of the year, with several officials suggesting that future rate hikes should be larger and remain higher for longer.

What’s the Fed’s Next Move?

No doubt, the slew of robust economic reports for January caught everyone, including the Federal Reserve, by surprise. Taken together, they indicate that a more muscular handoff to 2023 than thought a month ago is underway. If nothing else, the notion that the economy was already in a recession when the year started, something that many commentators – and some economists – firmly believed has been debunked. Barring a complete collapse in February and March, which is highly unlikely absent a major shock, the first quarter is on track to post a decent growth rate.

No doubt, the slew of robust economic reports for January caught everyone, including the Federal Reserve, by surprise. Taken together, they indicate that a more muscular handoff to 2023 than thought a month ago is underway. If nothing else, the notion that the economy was already in a recession when the year started, something that many commentators – and some economists – firmly believed has been debunked. Barring a complete collapse in February and March, which is highly unlikely absent a major shock, the first quarter is on track to post a decent growth rate.

The next Federal Reserve rate-setting meeting is scheduled for March 21-22, when another rate increase is all but certain. Both the Fed’s projection in December signaled that one is coming and recent comments by Fed officials, including Fed chair Powell, confirmed it. The only question Is whether it will match the smaller quarter-point increase triggered at the last meeting on February 1 or a bigger half-point increase that some of the more hawkish officials want because of the resilient inflation depicted by recent data.

There are still some key economic and inflation data coming out before the meeting takes place, including two job and consumer price reports. Should they surprise on the upside like they did for January, not only would the odds favor a larger rate hike, but the prospect of several more increases in following meetings would be on the table. Some economists already believe that the Fed’s policy rate, now in a range of 4.50-4.75 percent needs to rise above 6 percent at some point this year, which is far above the consensus expectation of roundly 5.5 percent.

Inflation’s Cooling, but Not Fast Enough

Although inflation was hotter than expected in January, it will not prompt a knee-jerk reaction from the Fed. For one, even with the month to month acceleration, the longer term trend is still cooling. Compared to a year ago, the consumer price index slipped to 6.4 percent in January from 6.5 percent in December marking the 7th consecutive month of slowing annual inflation. Likewise the core CPI, which excludes volatile food and energy prices, slipped to 5.6 percent from 5.7 percent. At the last Fed meeting and in follow-up comments, Chair Powell has said that the “disinflationary process is starting.” That observation continues to be valid.

Indeed, core goods prices declined in three of the past four months and are up only 1.3 percent over the past year. Last winter, these prices were rising by close to 13 percent. This dramatic cooling of goods inflation reflects several forces, including the shift in consumer buying habits towards services as the post-pandemic economy continues to reopen. Additionally, the supply chain snarls that restricted the availability of goods over the past two years have almost fully cleared up. That said, the positive contribution to lower inflation from the goods side has probably run its course.

Hence, continued progress on the inflation front will depend heavily on service prices, which continued to run far too hot in January, up 7.2 percent compared to a year ago. Service prices are much stickier than prices of goods, which are influenced by global supply and demand forces that often change rapidly. Service prices are primarily affected by domestic conditions, particularly by labor costs, which comprise the biggest expense for most service providers. Case in point is leisure and hospitality, such as restaurants, where labor shortages are particularly acute and wages have been rising faster than for most private-sector workers.

Focus on Jobs

Unsurprisingly, the Fed has been laser focused on the job market, convinced the inflation fight cannot be won until wages cool significantly. Depending on which of the numerous measures of wages is used, it is estimated that labor costs are rising within a range of 4.5-6 percent. The Fed thinks the increases need to be slowed to about 3.5 percent which, together with a 1.5 percent productivity trend, would be consistent with its 2 percent inflation target over time. The question is whether such a slowdown in wage growth can be accomplished without causing a massive increase in unemployment, something that would seriously weaken the bargaining power of workers.

From our lens, such a dramatic solution is unnecessary. For one, the current inflation upsurge has been driven mostly by Covid-related supply snarls and excess demand, fueled by pandemic-era savings not by wages. In fact, wage growth has been slowing since last fall. The increase in the Fed’s favorite labor cost measure, the Employment Cost Index which covers both wages and benefits, slowed to 1.0 percent in the final quarter of 2022 from 1.2 percent the previous quarter. The average hourly earnings data included in the monthly employment report has also been slowing. Simply put, the dreaded wage-price spiral that keeps the Fed up at night is missing the ignition key.

To be sure, the Fed is correct about the resilience in service prices, and is understandably perplexed over the economy’s rebound in January despite the dramatic climb in interest rates. But about 50 percent of the increase in the consumer price index in January was in the housing component, reflecting rising rents. The data for rents, however, is not current as it includes leases negotiated over the past year. According to housing industry sources, including Zillow, rents are either declining or barely increasing on new leases. In coming months, the recent trend will start to have a greater influence on the inflation index, pulling it down quite dramatically over the second half of the year. What’s more, many service prices are estimated by the government, particularly for medical care where profit margins in the health industry are used as a proxy for doctor’s fees. Similarly, many financial service prices are based off changes in the yield curve.

The skepticism over service prices can also apply to the strength in economic data in January, which can be heavily influenced by seasonal quirks around the turn of the year. The surprising rebound in retail sales, for example, may simply reflect less of a post-holiday pullback than usual because holiday sales in November and December were weak. Since the season adjustment factors looked for a bigger pullback, they gave the raw data more than a typical boost in January. The risk is that the Fed becomes overly influenced by what could be flawed data, spurring it to raise interest rates more than is necessary. As it is, the economy has not felt the full impact of the rate hikes already on the books, and the central bank may step harder on the brakes just when the economy is reeling from past hikes.